Money launderers are always finding creative ways to launder proceeds of crime without being exposed.

Money launderers go through considerable effort (and creativity) to disguise the proceeds of their activity under the cover of legitimate business activity. In addition, experience has shown us that money launderers are keen to exploit vulnerabilities inherent in enforcement systems, undertaking cross-border transactions using complex structures.

Malta is not immune to this. Our financial services sector has grown considerably over the past years, with Malta becoming an attractive country of choice for international investors. Our favourable taxation system, based on tax refunds upon dividend distribution to non-resident shareholders, has for the past years attracted significant interest and generated considerable investment. Over time, various holding and trading entities, some with limited substance, were incorporated in Malta. Consequently, Malta is now more at risk of being used as a channel to launder proceeds of crime where money launderers can blend funds from their illicit activities in legal transactions.

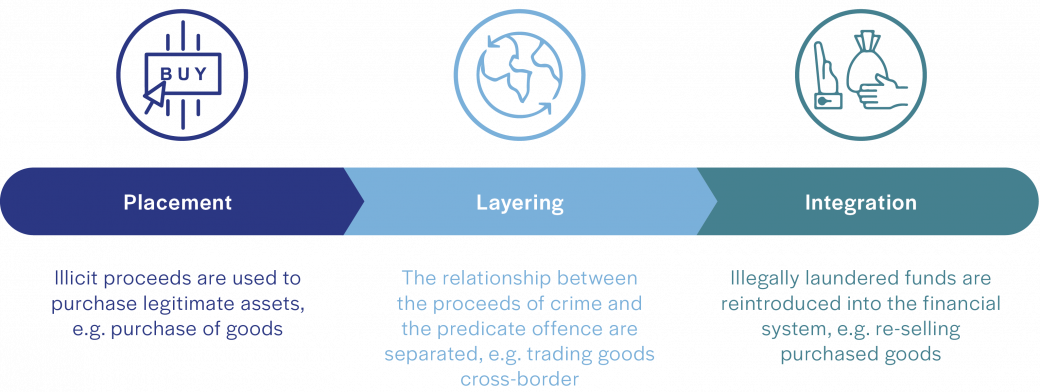

It would be very wrong to think that Malta’s attractiveness to money launderers lies only in its tax system. Paradoxically, money launderers may be very happy to be taxed. Their prime motivation is to distance the funds from their illicit activity (layering process) with the ultimate aim of integrating ill-gotten funds (albeit net of the laundering costs) into the financial system, in order for them to use and enjoy the proceeds.

From a Malta jurisdiction perspective, it is likely that if local accountants, auditors, tax advisors and corporate services providers had to encounter cross-border money laundering activity, this would typically be in the layering phase of the cleaning process.

What is trade-based money laundering?

The Financial Action Task Force (FATF) defines trade-based money laundering (TBML) as “the process of disguising proceeds of crime and moving value through the use of trade transactions in an attempt to legitimise their illicit origins”. As in many money laundering schemes, the focus is not on the movement of goods, but rather on the movement of funds. The movement of funds in a TBML scheme requires collusion between parties who abuse of trade finance services to facilitate the trading of goods. These schemes would usually involve professional money launderers, like for example lawyers and accountants, who offer their services to the beneficiaries of illicit proceeds of crime by providing their expertise to disguise the source of funds to avoid detection, in exchange for a fee or commission.

Goodwilled accountants, corporate service providers and lawyers may also unwittingly find themselves at the centre of a cross-border trade-based money laundering scheme. Understanding the purpose of business, married with professional scepticism and an eye for detail, are some of the main weapons practitioners have in their armoury. However, even these qualities may be impaired due to “familiarity” and “commercial interests” – money launderers and their agents have an artful and convincing way of blurring “objectivity”.

Typical red flags for accountants to look out for

The following is a non-comprehensive list of some of the more common traits that may indicate the existence of a trade-based money laundering scheme. It goes without saying that one swallow does not necessarily make a summer, yet the existence of some of these traits may require closer analysis. In doing so, subject persons must be careful not to fall foul of their tipping-off obligations.

The volume of goods being shipped appears to be much larger than the regular business activity;

Goods are transported from or to a high-risk jurisdiction;

The payment of goods is made by third parties who do not appear to have any connection with the transaction;

Goods being shipped are considered to be high-risk goods for money laundering, or goods connected to high-risk industries, like for example precious metals or equipment for the oil and gas industry;

Discrepancies between the description of goods on the bill of lading and those included in the invoice could mean a false description of goods, over or under-invoicing, or over or under shipping;

Goods are transported through jurisdictions or entities for no apparent reason;

The goods purchased are to be sold immediately, typically to one or a few customers, with a back-to-back type of arrangement;

Credit terms are provided loosely without the expected levels of commercial guarantees and security in place;

Credit terms do not elicit the commensurate commercial reaction expected in an arm’s length transaction;

The buyer and/or seller does not demonstrate the necessary experience and/or standing to carry out such a transaction. Desktop internet research renders limited information thereon.

Communications are typically not carried out directly with the buyer and/or seller but through an agent.

The article was written jointly byAlan Craig and Rebekah Barthet. Alan Craig is the advisory partner at Mazars in Malta, specialising in internal audit, governance, money laundering and regulatory compliance. Rebekah Barthet is a forensic investigation and compliance senior manager at Mazars in Malta, specialising in investigation assignments and regulatory compliance.

While traditionally subject persons have focused their efforts on the identification and verification of the customer and the underlying beneficial owner/s, less importance has been placed on understanding the Money Laundering and Financing of Terrorism (ML/FT) risk relating to the customer’s business activity, the source of wealth and the source of funds.

In today’s world of tightening regulations and an evolving risk landscape, companies are facing increased pressure to comply with Anti Money Laundering (AML) regulations to avoid hefty fines, reputational risk, and disruptions to their operations.

Want to know more?

Rebekah Barthet

Forensic investigation & compliance assoc director

Birkirkara

Our AML Compliance unit assists organisations by offering tailored support and solutions to meet their regulatory requirements. Our team includes Certified Anti-Money Laundering Specialists (CAMS) with extensive experience in the AML/CFT area.

Are you involved in a dispute or thinking about legal action? Our forensic team has extensive case experience and a proven track record in investigating financial and accountancy issues.